Climate policy is costly for firms: Evidence from the EU Carbon Border Adjustment Mechanism

The EU Carbon Border Adjustment Mechanism

Previous research: Why were the effects of EU climate policy limited?

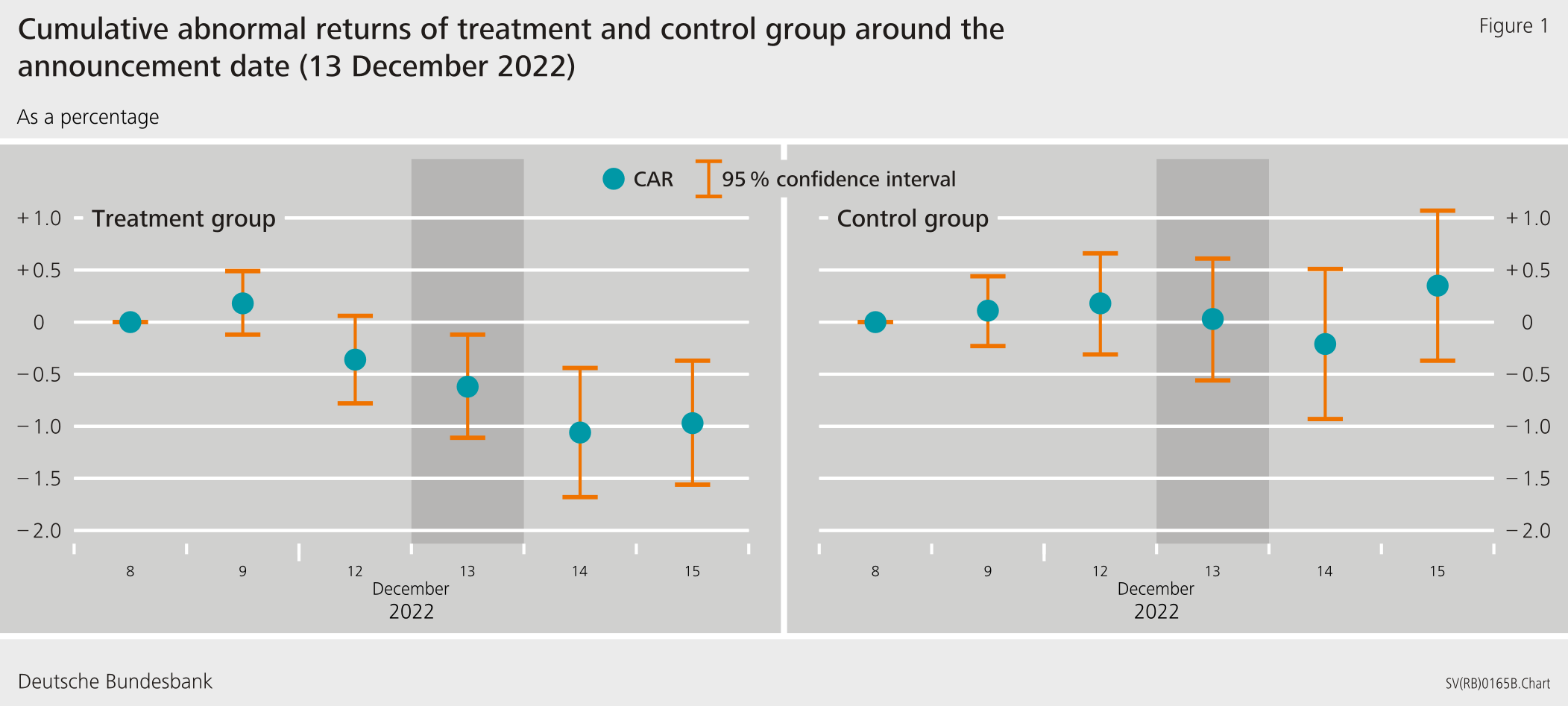

The announcement of the CBAM agreement had a negative impact on firms’ stock prices

Ex-post climate policy evaluation will shape our research agenda going forward

References

Authors

Mengjie Shi

Yupu Zhang

Christoph Meinerding

Disclaimer

The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem.